5. Not taking inflation into account

The simple definition of inflation is: The rate at which the general level of prices for goods and services is rising, and, subsequently, purchasing power is falling. One of the scary things about retirement is that our dollars will have less buying power in the future, and we will need more dollars in future to purchase the same goods and services.

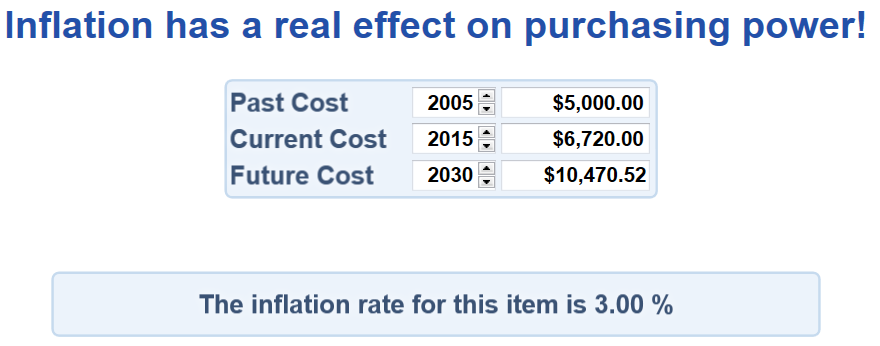

For instance – if we needed $5000 a month to live in 2005, and had a 3% annual inflation rate to today, we will be needing $6,720 per month to purchase the same amount of goods and services as we did in 2005.

Let’s say that someone is 50 years old today. With a 3% inflation rate, it means that in 15 years when they are age 65, they will need $10,470 a month to purchase the same goods and services as they did in 2005 with $5000

One BIG THING to consider then is, “Will I need less money in retirement than I need today?” In this case, to have the same lifestyle, I will probably need MORE. What about my taxes then, will I be in a higher or a lower tax bracket when I retire? The inflation calculation needs to be taken into account when considering this question.

What if inflation went to 4%? The number would shift to $13,329!

6. Relying on government and employer retirement plans

Many Employer Retirement plans are changing by the month and the burden is shifting more and more to the employee to provide for their own retirement. Corporate pensions are becoming more and more scarce as people live longer. [See Retirement Mistake #3]

Some big cities and municipal and service entities have filed for bankruptcy over the past few years which makes the future more and more scary for those relying totally on government and employer retirement plans. Detroit city, with total debts of $18.5 Billion is the largest city to date to file for bankruptcy. Prior to that, the record was held by Stockton CA with a debt of $26 million.

A good idea might be to plan for additional revenue streams separate from our current employer or government sources.

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship