To see questions 5-8 click HERE

To see questions 1-4 click HERE

The answers to these questions are different for each family and there are no right or wrong answers. Your family is unique and your needs are different from your neighbor.

All we want is for the parents and the student to be on the same page so that there are no surprises once the student has been accepted at the college of their dreams. It is always a lot better to have had some of these discussions way in advance in order to manage expectations.

- Do we have any idea of what our EFC number is?

Every week I have parents coming into our office seeking advice on College and Financial planning. When asked if they know what their EFC is most have no idea. A family’s Expected Family Contribution is a calculation made when you complete the FAFSA or Profile forms each year and it is the initial amount that most colleges will expect you to write on your personal check BEFORE you can get any need-based financial aid.

One of the first things we do, whether the student is a freshman or a senior, is to calculate the two types of EFC numbers for the family. This is the starting point of our discussions. From there we can establish how to begin our planning process.

This number is not the amount that you will pay for college, or the amount that you might get in financial aid, it is just the starting point of many calculations and discussions and families should know this number even if your student is in first grade and monitor the changes from there. Families will have a new EFC each year.

- Should I even complete my FAFSA form? – I have been told that I will probably not get aid.

Friends, neighbors, water cooler buddies – I constantly get people telling me that they have been told by others that they will not get any financial aid. Not all financial aid is need-based. Some schools try to attract high net worth families. How will they know that you are either in need or have High income or Net Worth if you have not completed the FAFSA form.

How will they know what your EFC is if you don’t complete the form? How will they know about all the competition that they have with other schools if they don’t see a big list of schools that you have applied to. [Many of these schools will allow you to apply without paying application fees]

How will they know that your student would like to apply for work-study programs if you have not completed the FAFSA form.

- Are we aware of the difference between the FM schools and the IM schools?

Some schools have different financial criteria when they look at a family’s profile to determine what college might cost that family. I had a family come in this week who had a Zero Federal Methodolgy EFC because of some circumstances, but their Institutional Methodology calculation was $36,000. They had no idea that there was a difference and their student had applied to both types of schools. This was going to have a huge impact on their ability to afford college.

Make sure you know what methodology the school uses, what financial factors make a difference, and what can be done about reducing that specific methodology so that we are not setting up false expectations for our students.

Don’t expect your school counselor to know this because they cannot ask you about your intimate financial circumstances, that’s not their job.

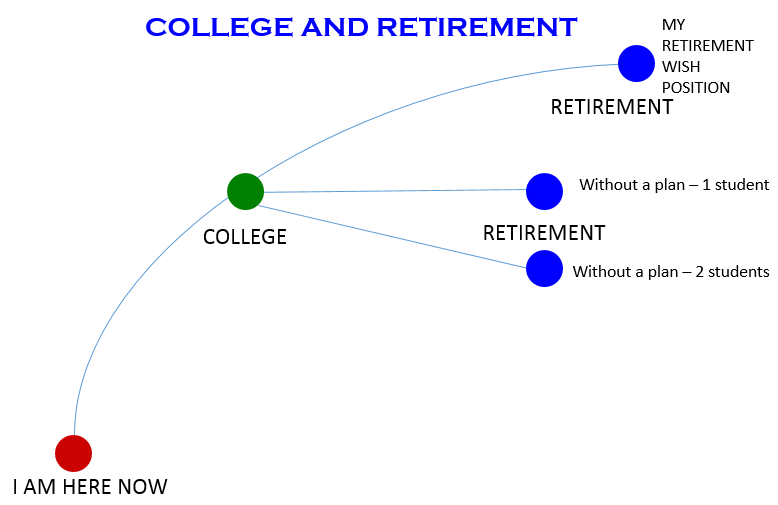

- How does this all fit into my retirement plans?

Look at this graph. You are at the lower red dot now and want to be somewhere else at retirement age.

There are a number of questions that need to be answered before we get there.

- At what age would I like to retire?

- How much do I need in my retirement accounts in order to live in the lifestyle that I want after retirement?

- Have I taken into account the expected longevity for both me and my spouse?

- Have I added inflation to that number?

- How much do I need to put away every year in order to achieve that retirement goal?

- What is the rate of return that I need to get in order to achieve that goal in the time I want?

- Is my family adequately protected should something happen to me before then?

If I do not have a definite plan for this, then HOW DO I KNOW HOW MUCH I CAN SPEND ON COLLEGE?

Remember, “Just because your student is leaving the nest, does not mean that they have to take your nest egg with them!”

Bonus question – What is the biggest mistake that people make?

They ASSUME that they cannot be helped. We have no idea whether we can help a family or not until we have a personal discussion with them to see what their unique circumstances are and then develop a personalized plan that it unique for their circumstances. Do the neighbors know your personal financial circumstances? Do your school counselors know what your retirement goals are and how the college choices will affect those?

The only way to know if a doctor can help is to actually go and see them.

These things are why we do what we do at College Planning America.

Contact us at davec@collegeplanningamerica.com or 714-813-1703

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship