By Dave Coen

Do you have a mortgage that you are repaying? If so, you can join the 63% of homeowners who have at least one mortgage to their name. (1) Many people struggle with the notion of whether to pay extra into their mortgage, or even to get a shorter term mortgage. In fact, the thought of not having a mortgage and then having all that extra money to use for other purposes might even inspire you to up your monthly principal payment, make a couple of extra payments a year, or come up with a plan to pay off your mortgage early.

That’s a noble endeavor, and one that very few people will fault you for, but is it really the best financial option?

Firstly, let’s just say that we would want your mortgage paid off as soon as you want it paid off, but perhaps in a more efficient way than most people are used to. There are some good reasons not to have a mortgage, but MANY good reasons why you should have one. I know that for many this thought might be a paradigm shift already.

Let’s look at just a few of the considerations that may help you make the right decision for your family.

The Growth Factor

Wherever you decide to put your money, you want it to work for you and give you the biggest payoff. That’s why one important factor when evaluating your options is that of growth. You might not want to put your extra money in a savings or checking account where you’re earning less than inflation because in effect you are then losing the buying power of your money. There is a battle between your mortgage interest rate and your expected investment return.

Firstly, let’s mention that if the interest rate is the same on both your mortgage and your rate of return on your investment, there is no difference on the final number that you would have in your pocket if the two rates are exactly the same.

Historically though, we are in a low-interest environment at the moment and the ability to lock in a low interest rate for 30 years could be a very positive thing.

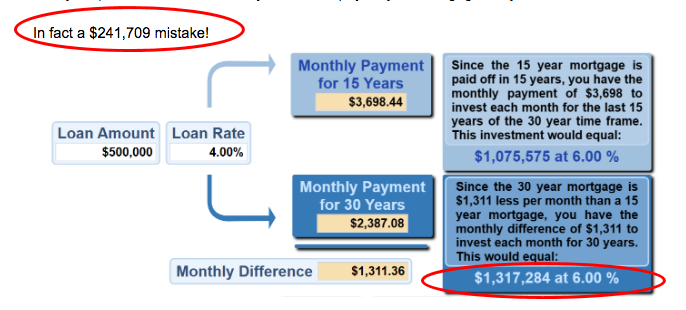

Let’s look at an example of a family with a $500,000 mortgage. If you have a mortgage rate today of 4%, and feel that you could average around 6% return in your investment account over the next 20 years, (the S&P has averaged 6.62% over the past 20 years to end 2018), then over a 30 year period it could be a costly mistake to pay off your mortgage early.

You know the rate of your mortgage, and it is usually fixed, so the one side of the equation is a given. This may sound simple on paper, but there are plenty of factors that could affect the outcome. And as we all know, even the best estimates aren’t guaranteed. It’s important to run a thorough analysis and consider taxes on investments, mortgage interest deductions, risk, and private mortgage insurance, among other elements of your financial life. An experienced financial advisor can run all of the numbers and conduct a complete examination of your unique situation.

It might not even be the numbers that are the greatest reason to go one way or the other.

The rate of return is just one of many things to consider though, and far from the most important one.

Mortgage Or No Mortgage?

Most financial gurus suggest that your mortgage not take up more than 28% of your monthly income. (2) But once you factor in other debt, in the form of student loans, auto loans, and credit card debt, plus additional living expenses, there’s often not much left to save. That’s why it’s tempting to think about putting all your extra resources into paying off your house, then directing all that money to savings once it’s paid off.

Liquidity is a significant pro for investing since you’ll have greater access to the funds in case of an emergency. If you put the money toward your mortgage, for all intents and purposes, it’s gone. The only way to get the money back is to sell your house or refinance your mortgage.

Taxes

When we rush to pay off our mortgages, we often underestimate how much we are giving up on the tax deduction benefits. There are usually more tax deductions in the first 15 years of a 30-year mortgage, than there are in the lifetime of a 15-year mortgage. Tax deductions could be significant in our calculations.

My House Value Is Growing

The growth in value of your house has nothing to do with whether you have a mortgage or not. Your neighbor’s house that has a big mortgage on it is growing at the same rate that the value of your house is growing at, whether you have a mortgage or not.

The MAIN REASON Why You Should Have A Mortgage – The LUC Factor

The LUC Factor means Liquidity, Use, and Control of your money. If you put the money toward your mortgage, for all intents and purposes, it’s gone. The only way to get the money back is to sell your house or refinance your mortgage.

There could be many reasons NOT to have a mortgage, but there are a few strong reasons to rather put the extra money into a side fund.

- Physical disability – If my income is affected by an illness, accident or some other disability, I can still keep up my mortgage payments if I have the side fund.

- What if I lose my job? If I have money in a side fund then I don’t have to lose my house to foreclosure and can still keep going until my income stabilizes.

- The uncertainty of the world – We all know of people who lost their houses after 9/11 or the market crash in 2008 because they did not have the cash flow to keep paying their mortgage. Many of these people could have kept their houses if they just had LUC of their money. They would have been much more secure if they had the side fund to keep paying their mortgage.

- I see too many people rushing to pay off their mortgages and then end up in retirement without enough money to live the way they want to. They have their house paid off but no access to money to live and end up having to borrow again when they have no job to make the payments, or be forced to sell their houses at a time when it might not be ideal for them to do so.

- Emergency need for cash – Many people find themselves paying their extra cash into their mortgage, and then needing cash in an emergency either for themselves or another member of their family. They then end up having to use credit cards at an exorbitant interest rate that ends up costing them way more than they intended.

Pay It Off In A Different Way?

Consider getting a 30-year mortgage, get all the tax deductions, the Liquidity, Use and Control, and pay the extra money that you might want to put into your mortgage into a side fund that is safe and preferably has tax-advantaged growth. Speak to your advisor to find what is suitable for your family.

In many cases you will find that in 15 years or less you will have the money in your side fund to pay off your mortgage. Then comes the BIG decision – If I HAVE the money to pay off my mortgage early, and I have the Liquidity, Use and Control in my side fund to do so at any time, would I WANT to pay it off?

How Do I Choose?

The above are just a few reasons NOT to pay off your mortgage early, but instead to save that extra money in a safe side fund. There are a number of other reasons for this that we would be happy to share with you upon request. There are several factors to take into consideration when choosing whether to use your excess money to pay down your mortgage or increase your investing. No one strategy fits everyone, but at SageView Advisory/College Planning America, our goal is to provide customized solutions that meet your needs and get you closer to reaching your goals. To learn more about how we can help you pursue the best plan for your family, email me at dcoen@sageviewadvisory.com or call 800-814-8742 / 714-813-1703 today.

About Dave

Dave Coen RICP® is a Financial Advisor with SageView Advisory and the CEO of College Planning America. Along with his retirement financial industry experience, he is a College Planning Specialist. He works closely with individuals and families to provide them comprehensive financial planning that addresses all elements of their financial picture. Learn more by connecting with Dave on LinkedIn.

1920 Main Street, Suite 800, Irvine, CA 92614 Tel: 800-814-8742

Registered Representative with Cetera Advisor Networks LLC, Member FINRA/SIPC. Advisory services offered through SageView advisory group, LLC. Cetera is under separate ownership from any other named entity. CA insurance license #0G82578

This material is designed to provide accurate and authoritative information on the subjects covered. It is not however intended to provide specific legal, tax, or other professional advice. For specific personal assistance, the services of an appropriate professional should be sought.

_________

(1) https://www.magnifymoney.com/blog/mortgage/u-s-mortgage-market-statistics-2018/

(2) https://www.investopedia.com/terms/t/twenty-eight-thirty-six-rule.asp

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship