Before we go through this, let me say that each family’s situation is unique, and I strongly suggest that you talk with a financial advisor before making any decisions.

The standard for calculations in communication from the Social Security Administration is an anacronym FRA or “Full Retirement Age” as per the Social Security Administration. For anyone born in 1960 or later, your FRA is 67. Right now, the maximum social security benefit at FRA is $3345 per month.

Generally, waiting to take your Social Security benefits will increase those benefits. With 67 being “FRA” that means taking Social Security before (e.g. Age 62), will reduce the benefits, and taking benefits later (Age 70) will increase those benefits.

Right now, benefits increase or decrease by 8% per year so the difference could be substantial.

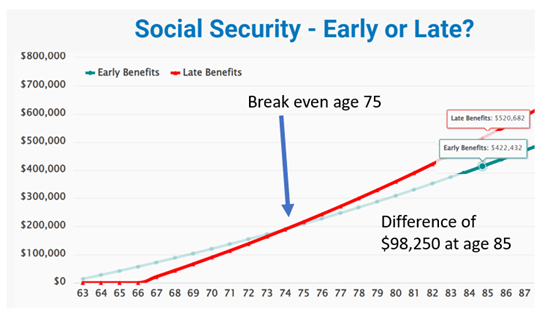

Let’s take a real example for someone aged 62 considering early SS rather than at age 67

In this scenario – If you think you will die before age 75 then better to take it early. Any date after that would be better to take it at age 67.

If you are considering taking SS at 62 in this scenario compared to age 70, then you would need to die before age 78 for it to be better to take SS at age 62.

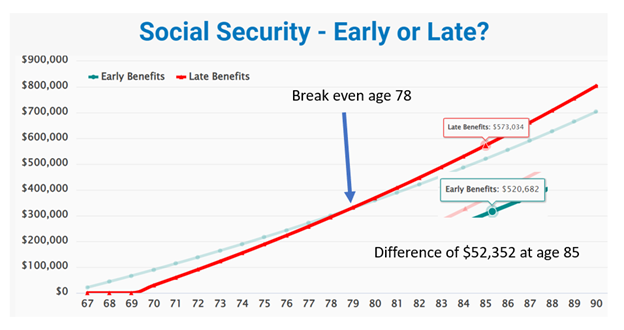

Let’s take a look at a consideration of SS at age 67 rather than at age 70

67 vs 70

In this scenario, if you think you will die before age 78 then better to take it early. If you think you will live longer than that, then it would be better to take it at age 70.

Possible reasons to take Social Security early.

- Health reasons – if you feel that you have reduced life expectancy.

- Widows or widowers can take survivor benefits as early as age 60. There are some options to claim a survivor benefit and then change to their own at FRA.

- It can sometimes make sense for the spouse with the lower benefit to claim before age 70 and then the higher-earning spouse waits until age 70. This could ensure that the spouse with the lower benefit would receive maximum survivor benefits if needed.

- If you are still working and receiving income, waiting to claim your benefits until FRA could be beneficial to avoid a reduction in SS benefits that can accompany earned income prior to FRA.

- Sometimes delaying tapping into your retirement accounts by taking SS before age 70 could allow tax-deferred assets to continue growing.

- If you are concerned about leaving a larger inheritance, it might be a consideration to claim SS earlier than 70, to reduce the withdrawals from assets. Perhaps if you have no spouse and are leaving your assets to children or other family members.

- If you have a pension where it could be beneficial to wait a while, then taking SS before age 70 could help with cash flow needs while waiting for your pension.

- If a spouse does not qualify for benefits of their own, or if their benefits are low, then they could qualify for 50% of the benefits of the higher-earning spouse. Remember that the higher-earning spouse needs to be already claiming their own benefits. If the spouse with the higher benefit is younger, then it could make sense for them to take their benefit earlier for the older partner to claim the spousal benefit.

- If you don’t need your SS benefit to cover monthly expenses, have a higher risk tolerance, and think that you can make more than 8% through investing your social security benefit, then you could consider taking your benefit earlier to invest that monthly amount to accumulate additional assets for retirement or leaving an inheritance. This method is at a higher risk and should be considered very carefully before implementation.

- If you retire before the age of 65, (Before eligible for Medicare) and need money to cover private health insurance and other out-of-pocket costs during this period, then claiming your SS earlier could help offset these costs.

- If your retirement date comes at a time when the market is substantially down, and you would prefer to wait until the market returns to a higher value, then claiming SS benefits before age 70 to delay drawing money out of your retirement accounts could give you some time for the markets to return.

In future blogs, we will cover some other subjects on Social Security:

How do I apply? What are the options for married couples? What about those divorced and spousal claims? Will we still have Social Security? What is the main problem?

How much is taxed? Is it indexed to inflation?

There are some good things about Social Security that make sense, and then some things that make you wonder – “Who’s idea was that?”

Let’s Talk

What is the biggest mistake that most people make? They ASSUME that they cannot be helped. We have no idea whether we can help a family or not until we have a personal discussion with them to see what their unique circumstances are and then develop a personalized plan that is unique to their circumstances.

Please feel free to contact me if you would like to discuss how we can help you with your family’s plan either in person, over the phone, or on Zoom

About Dave

Dave Coen is a Retirement Income Certified Professional (RICP®) and Financial Advisor with SageView Advisory, and CEO of College Planning America. Along with his retirement financial industry experience, he is a College Planning Specialist. He works closely with individuals and families to provide comprehensive financial planning that addresses all elements of their financial picture. Learn more by connecting with Dave on LinkedIn.

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship