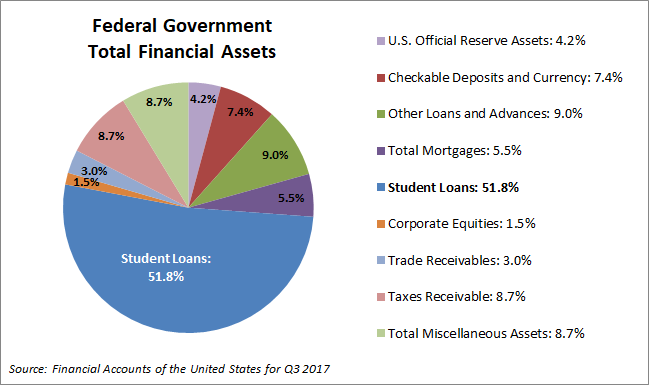

Pop Quiz – what line item is the largest asset in Uncle Sam’s financial accounts?

- A) U.S. Official Reserve Assets

- B) Total Mortgages

- C) Taxes Receivable

- D) Student Loans

The correct answer, as of the latest quarterly data, is … Student Loans.

This past week there has been an interesting article by Jill Mislinski in Advisor Perspectives. Article here

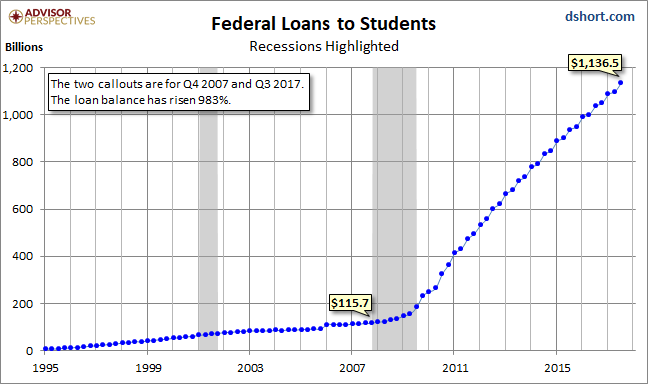

A stunning chart that continues to haunt us illustrates the rapid growth in federal loans to students since the onset of the great recession. The chart is based on the Federal Reserve’s Financial Accounts data (available here) for government’s assets and liabilities.

As pointed out on the chart, the two callouts are for Q4 2007, the quarter in which the Great Recession began (December 2007), and the most recent quarter on record, Q3 2017. The loan balance has risen an astonishing 983 percent over that time frame, most of which dates from after the recession.

This does not even take into account the amounts outstanding in PARENT LOANS!

This chart only includes federal loans to students. Private loans increase the debt burden. The Federal Reserve Bank of New York regularly tracks household debt and credit. In their most recent update, they calculate student loan debt to be nearing $1.36 trillion. Incidentally, the number of defaulted student loans hit a new high in 2016, according to a 2016 Time article.

But back to our quiz. Student loans may be a liability on the consumer balance sheet, but they constitute an asset for Uncle Sam. Just how big? It’s 51.8 percent of the total Federal assets. This is 9.4 times larger than the 5.5 percent for the Total Mortgages outstanding and about 6 times the size of Taxes Receivable at 8.7 percent.

The 51.8 percent referenced above is currently at its peak. Here is a look at how this metric has changed since 1995.

Of course, assets are, sadly, the trivial side of Uncle Sam’s Financial Accounts balance sheet — about 2.19 Trillion. The liability side totaled 18.87 Trillion at the end of Q3 2017.

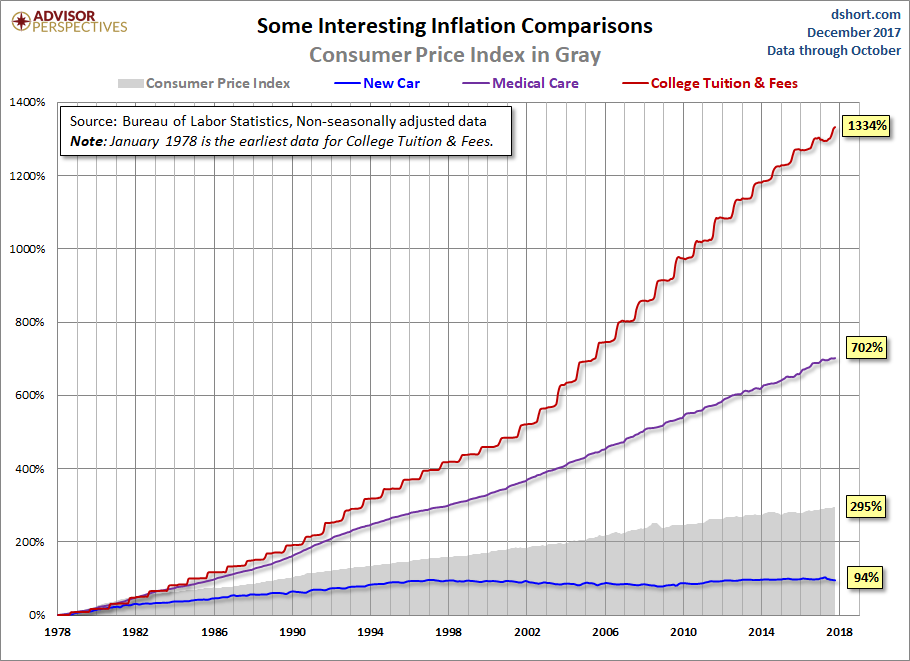

Here is a chart of data from the relevant Consumer Price Index sub-component reaching back to 1978, the earliest year Uncle Sam provides a breakout for College Tuition and Fees. As an interesting sidebar, we’ve thrown in the increase in the cost of purchasing a new car as well as the more substantial increase for the broader category of medical care, both of which pale in comparison.

During the decade of the 1990’s, when real out-of-pocket funding declined 25%, tuition and fees rose 92%, which sounds substantial … until you compare it to the 1334% across the complete data series. For early boomers paying for college was sort of like buying a car. But in recent decades, it has become more like buying a house, for which the strategy of a minimum down payment is commonplace for first-time buyers.

The student loan bubble, the biggest slice in Uncle Sam’s asset pie, will haunt us for many years to come.

We really need to help our kids make smarter decisions about their futures and discuss all options available to them. If this is the state of student loans, then I think that the state of loans that PARENTS have taken on for their students would stun us.

Whether it be for College Planning or Retirement Financial Planning, let’s PLAN

To schedule a time to meet with us please e mail davec@collegeplanningamerica.com or call 714-813-1703

Dave Coen RICP® is CEO of College Planning America and a Registered Representative at SageView Advisory

davec@collegeplanningamerica.com dcoen@sageviewadvisory.com

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship