A large part of what I do for a living is to assist families to assess their “Retirement Readiness”. The planning part obviously comes first, and this is called the Accumulation Phase of proper planning. If we have done a good job throughout this phase, then there will come a time for the big question.

“Are we OK to retire now?”

We then start planning the Withdrawal Phase. Obviously, this question should be planned for long before the retirement date, but there are a number of factors that should be taken into consideration. These factors should be part of conversations with your financial advisor early so that you can plan correctly.

Once you get to finally decide that “YES, I can retire”, then there are a number of things that we have to watch out for over the next 30 years or so in order to make sure that we maintain our lifestyle as we had planned for.

It is for this reason that I have put together this list. We will go through two of them in each newsletter. Think hat these are not for us yet? Perhaps we have parents that we might want to make sure are OK and not going through these challenges. We can also teach our kids – we cannot plan too early. Remember that if we don’t do this right, we are going to rely on our kids’ support one day.

Many of these might not cause catastrophic failure, but there are the BIG 5 that could, so pay close attention to those or they could have disastrous consequences.

- Not taking Inflation into account – This is one of the BIG 5

When working, inflation is often offset by an increased salary. In retirement, inflation reduces the purchasing power of income as goods and services increase in price, impeding the client’s ability to maintain the desired standard of living.

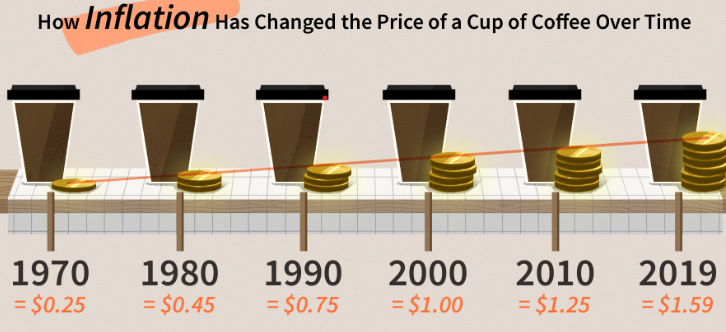

Inflation is a word that we have all heard for many years, and sounds so innocuous, but could have a dramatic effect later in life when it is too late to do anything about it. It is one of those factors that we cannot control, but we can plan for it.

Think about some of these things from 20 years ago:

- Toyota Camry then $17,898 now $24,425

- House value then $300,000 now $896,000

- Electricity bill then $200 now $327

- Average price of gasoline to fill a 16-gallon tank then $24.16 now $40.48

- Assisted Living costs 20 years ago cost then $55,000 now $100,000

- What cost a year in healthcare then$20,000 now $39,800

We will probably still need all these things 20 years into retirement, especially assisted living and medical costs. We surely don’t want our spouse to have to struggle through those years when we just cannot generate income anymore, or have our kids support us just when they are trying to put their kids through college.

So what does that mean for my planning? US government data expects inflation to average 2.2% over the next 20 years. When we do retirement planning for families, we work on a number of 2.5% so that we don’t underestimate and cause harm later.

That means that if I retire today at age 65 on $100,000 per year, then in 20 years, I should plan to have to withdraw:

At 2.2% inflation – $154,531 PLUS the extra taxes because I might be in a higher tax bracket

At 2.5% inflation – $163,861 PLUS the extra taxes because I might be in a higher tax bracket

That is 50 – 60% higher than my number today of $100,000

I also know that we can explain this away by saying, “I won’t need all of today’s money in 20 years” or “I will spend less in retirement than I do now”

Those statements don’t always take reality into account. I was speaking to a group of retirees a while back and asked them how many were spending less in retirement than when they were working – only one put up his hand. In many cases, this is because of inflation.

Before we decide to retire, get an analysis done from your advisor and then make sure we plan for this first “BIG 5”

Let’s Talk

Please feel free to contact me if you would like to discuss how we can help you with your family’s plan either in person, over the phone or on Zoom

About Dave

Dave Coen is a Financial Advisor with SageView Advisory and the CEO of College Planning America. Along with his retirement financial industry experience, he is a College Planning Specialist. He works closely with individuals and families to provide comprehensive financial planning that addresses all elements of their financial picture. Learn more by connecting with Dave on LinkedIn.

SageView Advisory – 1920 Main Street, Suite 800, Irvine, CA 92614 Tel: 714-813-1703

SageView Advisory Group, LLC is a Registered Investment Adviser. This message is for informational purposes only and is not a solicitation to invest. Advisory services are only offered to clients or prospective clients where SageView Advisory Group, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future results. No advice may be rendered by SageView Advisory Group, LLC unless a client service agreement is in place. CA insurance license #0G82578

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship