In our previous newsletter, we looked at the impact of inflation, a Big Thing, and Ponzi Schemes on retirement planning.

The next two are more about our portfolios.

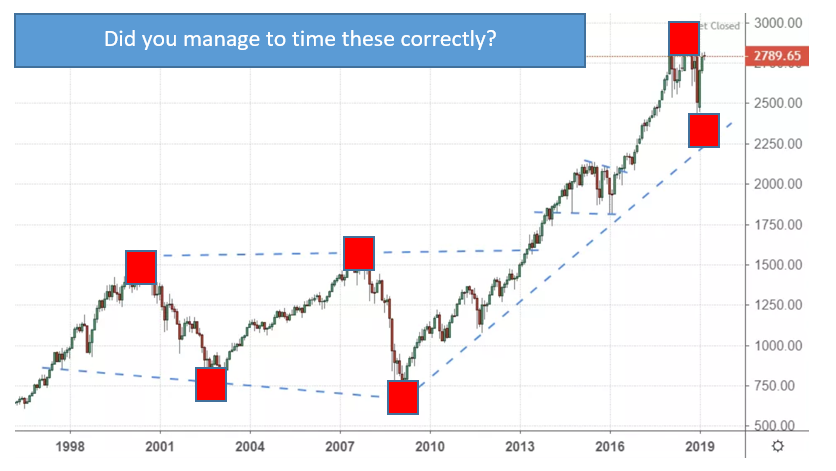

#4 Attempting to time the market

The past 6 months should be a great example of the risks of trying to time the market. There are circumstances that can occur that some people can predict, and then others that nobody can predict that could cause the market to go both up and down.

Trying to time the market means buying low and selling high. The problem is that you have to be able to predict each of those and then act on that. Many “Experts” have tried over many years to time the market but most have failed.

After a drop in the market, there is sometimes a quick recovery, and other times it could take a while. The other consideration to take into account is that if I am to buy low, I have to have the cash available at the time to buy into the market when I think it has reached it’s low point. Most people end up losing out on growth on that cash while waiting for the market to drop. Think about it – if I really knew when the market was going to fall, have I previously sold my positions before the market drops in the past? If the market has fallen, did I actually commit my cash INTO the market before it went up again? If I managed to get that right, is that because of great analysis or pure luck?

Research shows that a large percentage of supposed “Experts” on TV or in other places get this wrong.

For a long term investor, it might be prudent to invest in a well-diversified portfolio that would see us through the ups and downs. If the market drops and our portfolio is down 20%, it is often wiser to wait and stay invested. (Assuming you have a properly diversified portfolio to start with) Obviously past performance is never indicative of future actions, but history has shown us that in the long term the market has done pretty well for patient and well-planned investors.

#5 Not diversifying correctly

While we are talking about having a well-diversified portfolio, let’s take a look at some of the various aspects we should consider when crafting such a portfolio and the types of investments that could be included.

Stocks – Individual stocks, Mutual Funds, ETF’s, Large Cap(Growth or Value), Med Cap (Value or Growth), Small Cap (Growth or Value), Non-US Dev, Non-US Emerging.

Bonds – Inv Grade, High Yield, Non US, Muni, other

Cash, Real Estate, Commodities

Then, within the Stocks – what sectors? (Cyclical, Sensitive, Defensive) Base Material, Financial, Services, Community Services, Energy, Industrial, Technology, Healthcare, Utilities

Where in the world? US, North America, South America, Europe Developed, Europe Emerging, Africa, Asia, Middle East, Japan, Australasia.

Then, what % within the portfolio, what duration on the bonds, what is my risk factor, what is the experience of the fund manager, Gross Expense Ratios?

Then there comes rebalancing – when to do it and how?

I think you get the drift – this is a little more than the average investor is probably knowledgeable on.

This is the reason why most people enlist the help of licensed, experienced, fiduciary financial professionals.

Please feel free to contact Dave Coen davec@collegeplanningamerica.com if you would like to discuss how we can help you with your family’s plan either in person, over the phone, or on Zoom.

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship