In our previous blog, we looked at market timing and not diversifying correctly.

The next one is important to be considered on its own.

- Not planning for “Sequence of Returns” – This is one of the “BIG 5” mistakes

Most people are focused on the Accumulation Phase where we are saving towards retirement and adding to our accounts. One of the facets that could be devastating to our retirement plans is when and how much we withdraw money.

This might not seem important for now if you still have many years to go before retirement, but if you have the ability to plan for it 20-30 years in advance, it could be a HUGE advantage when you might face this challenge in later years.

This is a retirement risk that could be eliminated in large part with proper planning and the “mistake” comes when people did not have information about it years in advance – you are no longer one of those.

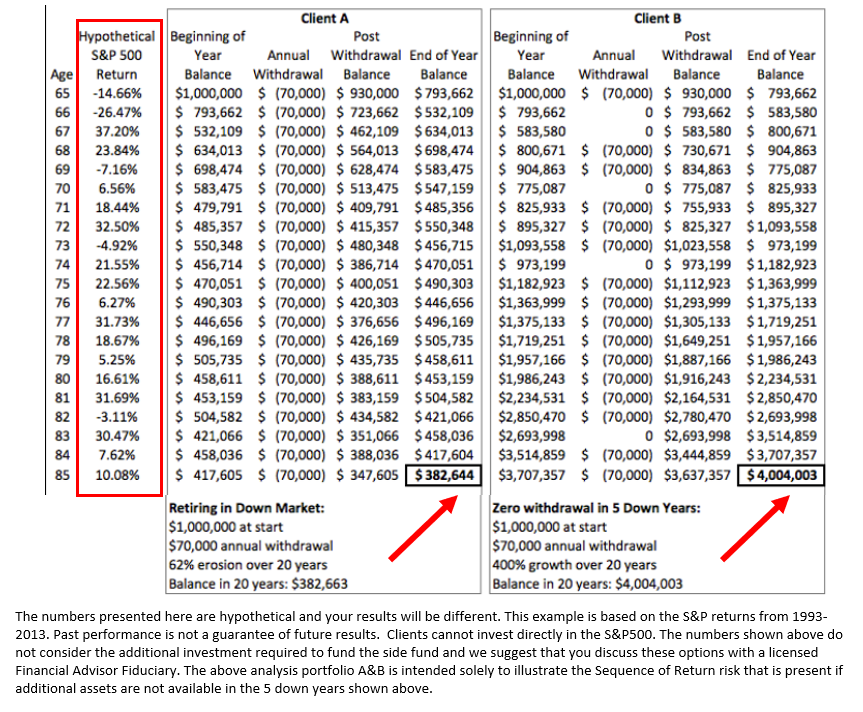

Investment returns are variable and unpredictable. The order of returns has an impact on the how long a portfolio will last if the portfolio is in the distribution stage and if a fixed amount is being withdrawn from the portfolio. Negative returns in the first few years of retirement can significantly add to the possibility of portfolio ruin.

The ”Fix” for this is fairly simple and involves funding an alternate account that is not reliant on the stock market at the time. There are various accounts that would facilitate this and I suggest that you discuss with your advisor to see which strategy is best for your family and your goals.

Let’s take a look at an example.

Client A and Client B both have $1000,000 at the start of their retirement and want to draw out $70,000 a year. Client B has a separate account that is not influenced by the stock market. There are various options that would be suitable for the separate account, and I suggest that this becomes part of your discussion in your personal Financial Plan. Some accounts could be more suitable than others based on your personal circumstances.

As you can see, in the “Down” years, Client B has the option of not making withdrawals from his account and funding his lifestyle from a separate account. Withdrawals are $350,000 less, but the difference in end-value is over $3million. There is no rate of return that can beat proper planning for this.

These are some reasons why we recommend the help of a licensed, experienced, fiduciary financial professional. Please feel free to contact me at dcoen@sageviewadvisory.com if you would like to discuss how we can help you with your family’s plan either in person, over the phone or on Zoom.

Dave Coen | RICP® I Registered Representative | SageView Advisory Group Tel: 714-813-1703 t (800) 814-8742 e dcoen@sageviewadvisory.com www.sageviewadvisory.com This material is designed to provide accurate and authoritative information on the subjects covered. It is not however intended to provide specific legal, tax, or other professional advice. For specific personal assistance, the services of an appropriate professional should be sought. A diversified portfolio does not assure a profit or protect against loss in a declining market.

SageView Advisory Group, LLC is a Registered Investment Adviser. This report is for informational purposes only and is not a solicitation to invest. Advisory services are only offered to clients or prospective clients where SageView Advisory Group, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future results. No advice may be rendered by SageView Advisory Group, LLC unless a client service agreement is in place. CA insurance license #0G82578

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship