Regardless of whether your child is two or twelve, the thought of college has probably crossed your mind. In the busyness of life and never-ending financial pressures, it is all too easy to put saving for college on the back burner. But one thing in life is certain; time moves quickly. Don’t get caught unaware and unprepared for college. Your child’s education is one of the most important investments you can make, and with today’s costs, it pays to plan ahead. Here are five steps that will get your plan off on the right foot:

1. Know What to Expect

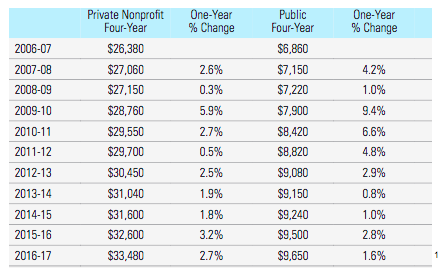

The numbers might cause you to break out in a sweat. Tuition rates have increased at a faster pace than many other items over the past decade and it doesn’t look like they will slow down in the next few years. Over the past ten years, college costs have risen an average of 2.4% a year for private schools and 3.5% for public colleges. Longer term, there could be some dramatic changes coming in the future due to technology.

If this upward trend continues, in 25 years it could cost $300,000 to obtain a four-year undergraduate degree. The costs will vary depending on the institution attended, room and board, and other educational expenses, but either way, that’s a pretty penny for four years of school. For a 2017 graduate, the average student loan balance was over $37,000 (2) and the average monthly student loan payment is $351. (3) For students just beginning their careers, that’s a hefty bill to pay. The substantial cost may seem overwhelming, but knowing what to expect gives you a goal to aim for. The flipside is that there is a strong possibility of alternate education in the future that would enable students to gain the necessary knowledge and skills to prepare them for the workplace that might look very different from the standard on-campus 4-year college. There are already many schools starting to embrace technology and alternatives.

2. Start Early

It’s never too late or too early to start saving for your child’s college fund. By starting early, you will reap the rewards of compound interest. (4) If you wait, your account balance may not be as high, but you are still investing something into your child’s future. Even if you don’t think you have enough room in your budget to add another line item, $25 a month is still $25 more than $0. Setting up automatic contributions is a good way to remind yourself that college is getting closer and your monthly account statement will keep this goal in the forefront of your mind.

3. Don’t Try to Pay For Everything, or All at Once

While some people are able to save and pay for the total cost of their child’s college education, most people don’t fit into this category. Even if you could, the questions is “Should I”. Just because college is 4 years, does not mean to say we have to pay it over 4 years. Not only are there many scholarship programs that you can take advantage of, but proper planning long before completing the Free Application for Federal Student Aid (FAFSA) could save tens of thousands of dollars. No matter what your income and asset status is, prior planning years ahead could increase your eligibility to the 3 types of Financial Aid and improve college affordability.

4. Choose the Right Way to Save

The most common methods people use to save for college is through a 529 plan or a Roth IRA. Although these are the two most commonly used, they might not be the best vehicles for everyone. Sometimes these two could end up being costly vehicles later on so each family might want to plan according to their own circumstances and goals with proper advice.

529 Plans

529 Plans are not good, and they are not bad. They are just another financial club in the bag and should be considered carefully before using. See – 529 plans-6 vital things I need to know

A 529 plan is a state-sponsored education savings account that allows earnings to grow on a tax-deferred status.

Every year, Morningstar publishes their list of the best and worst college savings plans which will help you make an informed decision and find a plan that will work for you.

529 plans can be a little complicated and could negatively impact financial aid. It also matters as to who owns the plan.

For example, if the 529 is owned by a grandparent, distributions count as untaxed income to the student. If they are disbursed in the first or second year of college, the disbursement can reduce eligibility for need-based aid by as much as 50% of the amount of the distribution. If the plan is reported as a parent asset or a student asset, it will reduce eligibility for need-based aid by much less, up to 5.64% and 20% respectively.

In addition, you can only spend the dollars from a 529 tax-free for certain college expenses. For example, computers qualify, but tablets and mobile devices do not. Paying for college qualifies, but paying for college loans does not. The new tax law introduced in 2018 has some positive attributes for parents who already have 529 plans and who pay for their student’s high school education.

Roth IRAs

Like 529 plans, Roth IRA’s have both positives and negatives. In recent years, Roth IRAs have gained popularity for things other than retirement due to their flexibility. Your Roth contributions can be withdrawn but have some limitations on timing, and can be used for any purpose. In addition, if managed correctly, Roth IRAs can help you avoid the high fees that some 529 plans charge and they also offer increased investment options. IRAs will not have any impact on your financial aid eligibility.

For college savings, Roth IRAs aren’t the perfect option, but they do offer an alternative to the traditional 529 plans. Often a multipronged strategy is the best fit for a family’s needs and might include a “Lifetime Learning account” which is being considered by congress at the moment. It’s best to get advice on savings strategies from a professional who is familiar with College Planning, while taking into account the whole financial picture and family goals.

5. Stay On Top of Things

Just like your 401(k) plan, you need to monitor these investments. While in the early days of saving for college you will want to be more aggressive with your investments. As college draws closer, the investment allocation should become more conservative, just like a retirement account. It is also helpful to monitor your balances, keep an eye on the changing college costs, and track your progress towards your goal.

How We Can Help

Planning for College could be one of the most important teaching moments we have with our kids to date. How we handle this could influence their decision-making process for the future. Each family is in a different stage of financial readiness for the huge expense of college. At College Planning America, we understand this and provide guidance which helps our families avoid the most common and costly mistakes while planning to finance college. Our team offers help to each family on how to maximize their financial aid options, minimize out of pocket costs and structure their finances to plan for college without jeopardizing their retirement in the process. If you are ready to create an A+ college plan, get started by emailing me at dcoen@sageviewadvisory.com or calling 714.813.1703.

About Dave

Dave Coen is a Financial Advisor with SageView Advisory and the CEO of College Planning America. Along with his financial industry experience, he is a College Planning Specialist and has served on the advisory board of a national College Planning training organization. He works closely with individuals and families to provide them comprehensive financial planning that addresses all elements of their financial picture. Learn more by connecting with Dave on LinkedIn.

1920 Main Street, Suite 800, Irvine, CA 92614 Tel: 800-814-8742

Registered Representative with and securities offered through Cetera Advisor Networks LLC (doing insurance business in CA as CFGAN insurance agency), Member FINRA/SIPC. Cetera is under separate ownership from any other named entity. CA insurance license #0G82578

________

(1) https://trends.collegeboard.org/sites/default/files/2016-trends-college-pricing-web_0.pdf

(3) https://studentloanhero.com/wp-content/uploads/Student-Loan-Hero-2017-Student-Loan-Statistics.pdf

(4) https://www.businessinsider.com/amazing-power-of-compound-interest-2014-7

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship