I get many questions on whether to borrow for college, and if so what sort of loans to take out to fund College.

The #1 biggest regret that students have AFTER college is the payments they have to make for years afterward, and the large amount of debt they are left with after college.

Obviously, the best option is to never have student loans, but if you are going to need to borrow money to pay for college, then it would be good to know what the options are and what the costs might be.

Perhaps I could mention here first – Most people think that the place they will save the most money for college is “Grants and Scholarships” Although that is definitely a factor, what I have found in my experience in dealing with clients is that most money is eventually saved through “Careful and planned decision making.”

Let’s look at the loan options.

Timeline:

Most colleges will ask students to pay in advance per semester, with the first bill being issued in July and typically due in August. Most spring semester bills are due in December.

Sometimes there are options to pay monthly, but that could increase the price and those payments could start in June. Student Loan providers often take between 1 and 5 days to process an application and issue a disbursement.

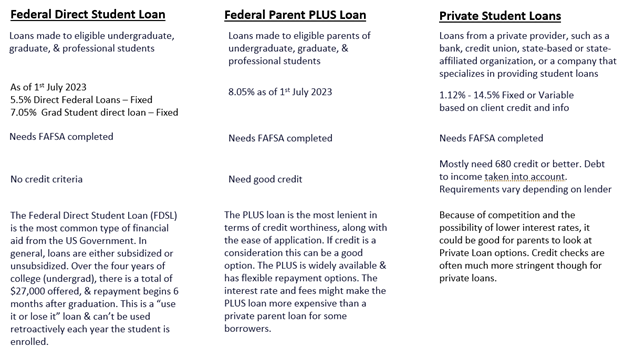

Federal Direct Student Loans

There are two types of Direct Federal Student Loans – Subsidized and Unsubsidized

Subsidized means that no interest accrues while studying. Payment starts after completion of full-time study.

Unsubsidized means that interest does accrue from disbursement even though payment will only start after completion of full-time study.

There is a limit to what the government will lend to a student for an undergrad degree, without asking the parents to co-sign on the loans, and then that becomes a different type of loan.

Currently, the maximum that a student can borrow on their name is $27,000 and they must secure the loan each year that they are enrolled.

These loans are disbursed as follows:

$5,500 – Freshman year

$6,500 Sophomore year

$7,500 Junior year

$7,500 Senior year

Once completing the FAFSA form and being accepted at a college, the student will receive notification as to what Federal loans they qualify for. Subsidized loans are only available to undergrad students, and usually, a mixture of the two is offered.

Unsubsidized loans are also available to grad students, have higher borrowing limits, and are not subject to financial need stipulations.

Federal Parent PLUS loans

PLUS loans are government loans to the parents of students provided by the Dept of Education.

PLUS loans are also available to graduate students without parents co-signing.

To be eligible for a federal plus loan you must have a good credit history and be a parent of a dependent undergrad student studying at least half-time at an eligible school.

Parents can borrow up to the cost of attendance for their student, minus any other financial aid.

Private Loans

These loans are offered by 3rd party lenders.

There are many private lenders offering loans, and perhaps a good website to look at is HERE

Generally, these are offered by banks and credit unions and have options for both fixed and variable credit rates.

There is a range of borrowing amounts, and these are not need-based but credit based, and you also could have the option of having a co-signor.

As a financial advisor, just a note of caution here. Although as parents we would be willing to give our lives for our kids, the question would be “Should we?” Applying for college is a wonderful opportunity and teaching moment for our kids to learn about the decisions we get to make in life and the consequences for many years later in life of those decisions.

Perhaps remember that our students can borrow for college that they will have to repay, but parents cannot borrow for retirement.

Let’s Talk

What is the biggest mistake that most people make? They ASSUME that they cannot be helped. We have no idea whether we can help a family or not until we have a personal discussion with them to see what their unique circumstances are and then develop a personalized plan that is unique to their circumstances.

Please feel free to contact me if you would like to discuss how we can help you with your family’s plan either in person, over the phone, or on Zoom

About Dave

Dave Coen is a Retirement Income Certified Professional (RICP®) and Financial Advisor with SageView Advisory, and CEO of College Planning America. Along with his retirement financial industry experience, he is a College Planning Specialist. He works closely with individuals and families to provide comprehensive financial planning that addresses all elements of their financial picture. Learn more by connecting with Dave on LinkedIn.

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship