1. Not saving enough apart from my 401K – This one is pretty obvious, the more we save the better we will be off in Retirement.

Too many people are relying ONLY on their 401K savings, but in many cases, even putting away the maximum we are allowed to into our qualified accounts will not give us enough to retire on alone.

In addition, having a diversified portfolio might be a wise choice, not in terms of the allocations inside of our qualified plans, but in terms of whether we want all our money in a tax-postponed bucket, or perhaps some in a tax-advantaged bucket.

Especially early on in life, as young folk start off earning money in what would typically be a low tax bracket, it might make sense to have some money growing in a bucket that will never be taxed again.

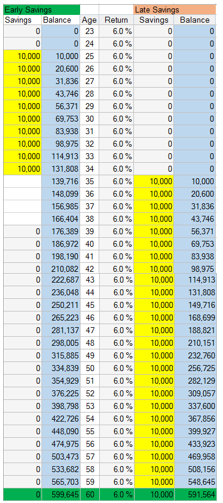

2. Starting our saving too late in life. The illustration below shows the huge benefit that we have if we start saving early compared to waiting. This example shows a young couple earning an actual 6% return saving $10,000 a year at age 25 for just 10 years and then NOTHING, compared to a couple waiting until they are 35 and then have to save $10,000 a year for the next 26 YEARS to get similar results.

We really need to start saving as early as possible ourselves and then encouraging our kids to do the same as soon as they get out of college. That way they will be far better off than most adults are today.

They do not have to start with $833 a month [The $10,000 a year we were talking about], but any amount would be better than waiting.

Stay tuned for more of the Ten BIG mistakes that people make with retirement planning

Apply for a College Planning America Scholarship

Apply for a College Planning America Scholarship

Speak Your Mind